For millions of Americans with FICO scores below 580–600, the door to conventional credit remains stubbornly shut. Every year, banks and credit unions reject a sizable chunk of applicants who could otherwise meet basic income and employment criteria. The result is a scramble for high‑interest payday lenders or no‑credit‑check installment loans that can trap borrowers in a cycle of debt.

Enter RadCred’s 2026 platform, an AI‑driven loan‑matching service that bypasses the rigid FICO gatekeeping many lenders use today. By evaluating over one hundred financial data points—bank transaction patterns, gig‑economy earnings, recurring spending habits and more—RadCred offers a nuanced view of a borrower’s repayment capacity without a hard credit pull.

In this article we explore how RadCred’s approach fits into the broader landscape of bad‑credit financing, what it means for consumers, and how a newer player like

Jetzloan can provide an alternative pathway to responsible credit building.

The Rise of AI in Credit Decisioning

Artificial intelligence has long promised smarter, faster underwriting. Traditional banks still rely heavily on static credit scores and income statements, which often fail to capture the full financial picture for gig workers or those with limited credit history. RadCred’s platform, unveiled March 24, 2026, leverages machine learning algorithms that process real‑time data from bank feeds, payroll APIs, and even social media activity to estimate a borrower’s risk profile.

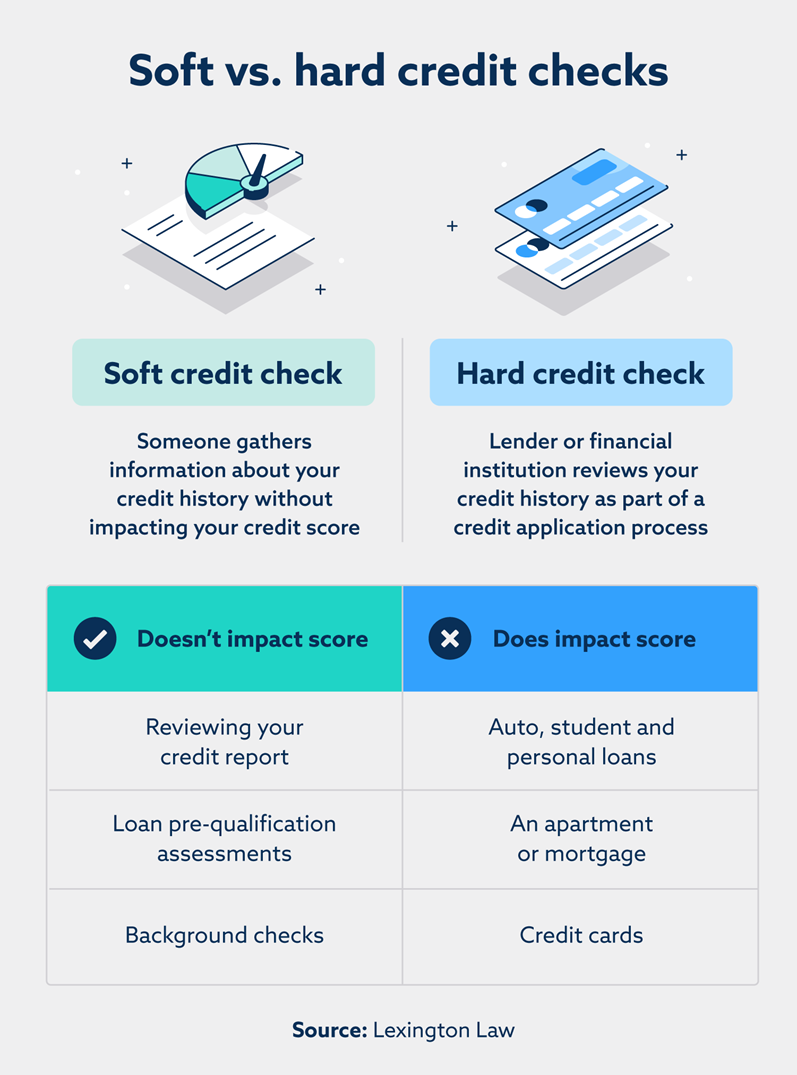

Unlike hard pulls that can ding a score, RadCred performs soft inquiries during the prequalification stage. This means consumers can explore loan options without affecting their credit health—an essential feature for those already grappling with low scores.

- Data Points Evaluated: Bank transactions, recurring deposits, employment stability across traditional and gig roles, verified income streams (wages, self‑employment, Social Security, disability), debt‑to‑income ratios from actual spending data, and recurring spending habits.

- Outcome Transparency: Full APR disclosure and upfront cost breakdowns are provided before any commitment is made.

- Regulatory Compliance: Loans are offered only through state‑licensed lenders, ensuring adherence to local lending laws.

These features align with growing consumer demand for “smart” financial products that adapt to non‑traditional income streams and provide clearer cost visibility.

How the Matching Process Works

Potential borrowers start by filling out a brief online questionnaire. The platform’s AI then cross‑checks the data against its lender network. Because RadCred is a matching engine rather than a direct lender, final loan terms—including interest rate, repayment schedule and funding speed—depend on each lender’s decision.

The process typically takes minutes, with same‑day or weekend funding possible through participating lenders. However, it’s important to note that while prequalification uses a soft pull, final approval may involve a hard inquiry from the chosen lender.

Consumer Impact: A Double‑Edged Sword

For borrowers who would otherwise be denied by banks, RadCred offers a lifeline. But the platform also highlights key considerations:

- Interest Rates & Fees: While often lower than payday loans, some installment options still carry high APRs that can erode savings.

- Repayment Terms: Shorter repayment periods may lead to higher monthly payments, straining budgets.

- Credit Building: Responsible use of a matched loan can help rebuild credit if reported accurately to the major bureaus.

Ultimately, RadCred’s model empowers borrowers with choice and transparency—critical ingredients for financial empowerment in a post‑pandemic economy.

Comparing RadCred With Other No‑Credit‑Check Options

Traditional no‑credit‑check loans often come from payday lenders or high‑interest installment companies. These options tend to have the following characteristics:

| Feature |

Payday Lenders |

RadCred Matchers |

| Interest Rate (APR) |

200%+

(often 400–600%) |

30–50%

(varies by lender) |

| Loan Term |

2–4 weeks |

3–24 months |

| Application Process |

Fast, minimal checks |

AI‑based prequalification

(soft pull) |

| Reporting to Credit Bureaus |

Rarely reported |

Often reported if lender chooses |

| Funding Speed |

Same day or next business day |

Same day or weekend, depending on lender |

RadCred’s AI‑matching sits somewhere between these extremes—offering higher repayment flexibility than payday lenders while still providing a more accessible entry point for those with low credit scores.

What Consumers Should Look For When Choosing a Loan

- APR Transparency: Ensure the lender discloses all fees upfront. Hidden charges can inflate the true cost dramatically.

- Repayment Terms: Longer terms lower monthly payments but increase total interest paid.

- Pre‑Qualification Process: A soft pull is preferable if you’re still shopping around.

- Reporting Practices: Verify whether the lender reports to all three major credit bureaus.

With these criteria in mind, consumers can weigh their options more effectively and avoid predatory pitfalls.

The Role of Jetzloan in a Changing Credit Landscape

While RadCred’s platform has garnered attention for its AI capabilities, smaller fintech firms like

Jetzloan are carving out niches by focusing on transparent, consumer‑friendly loan products. Jetzloan offers short‑term personal loans with fixed interest rates and no hidden fees, appealing to those who want a straightforward borrowing experience.

Unlike many high‑rate lenders that use aggressive marketing tactics, Jetzloan’s business model emphasizes:

- Clear Rate Disclosure: APRs are presented upfront without surprise add‑ons.

- No Prepayment Penalties: Borrowers can pay off loans early without incurring extra costs.

- Fast Funding: Funds typically arrive within 24 hours of approval.

For borrowers navigating a world where traditional banks remain inaccessible, Jetzloan provides a viable alternative that balances affordability with ethical lending practices.

How to Apply Through Jetzloan

- Visit the website: Enter personal details and desired loan amount.

- Submit proof of income: Acceptable documents include recent pay stubs, tax returns or bank statements.

- Receive instant decision: The platform uses a lightweight algorithm to provide real‑time approval status.

- Accept terms and receive funds: Once accepted, funds are deposited directly into your account.

This streamlined process mirrors the efficiency seen in RadCred’s AI matching while maintaining transparent pricing—an attractive proposition for consumers seeking reliable credit solutions.

Regulatory Environment and Consumer Protection

The rise of fintech loan platforms has prompted increased scrutiny from regulators. The Consumer Financial Protection Bureau (CFPB) and state banking departments are actively monitoring both AI‑based lenders and traditional payday operators to ensure fair practices.

- Soft vs Hard Pulls: Consumers can now compare how each lender handles credit inquiries, which can affect their score differently.

- Fee Caps: Many states have implemented limits on fees for short‑term loans to curb predatory lending.

- Transparent Reporting: Regulators are pushing for mandatory reporting of loan performance and repayment history to credit bureaus.

These regulatory changes aim to level the playing field, giving borrowers clearer information to make informed decisions. Both RadCred and Jetzloan have positioned themselves as compliant entities, offering consumers peace of mind in an evolving market.

Future Outlook for Bad‑Credit Lending

As AI technology matures, we can anticipate further innovations:

- Dynamic Credit Scoring: Models that adjust risk assessments in real time based on payment behavior.

- Blockchain Verification: Securely verifying income and employment data to reduce fraud.

- Embedded Finance: Integrating loan offers directly into everyday apps, like banking or budgeting tools.

These advancements will likely increase accessibility for consumers while maintaining responsible lending standards—an outcome that both RadCred and Jetzloan are poised to capitalize on in the coming years.

Key Takeaways for Borrowers Seeking Credit

- AI‑powered platforms like RadCred provide a more nuanced assessment than traditional credit scores alone.

- Soft pulls during prequalification allow consumers to shop without harming their score.

- Transparent, fixed‑rate loans from firms such as Jetzloan offer an ethical alternative to high‑interest payday lenders.

- Regulatory oversight is improving consumer protection across the fintech space.

- Staying informed about APRs, fees, and repayment terms can help borrowers avoid costly debt cycles.

With these insights in hand, consumers can navigate the complex landscape of bad‑credit lending more confidently, leveraging technology to secure fair, manageable financing solutions that align with their long‑term financial goals.